Before we start comparing vendors, give me a minute to set the baseline.

A core banking system is the operational engine of the bank. It handles accounts, transactions, payments, lending, deposits, customer records, reporting, and ledger operations. Every time a customer transfers money, checks their balance, repays a loan, or receives a payment notification, the core platform is involved somewhere in that process.

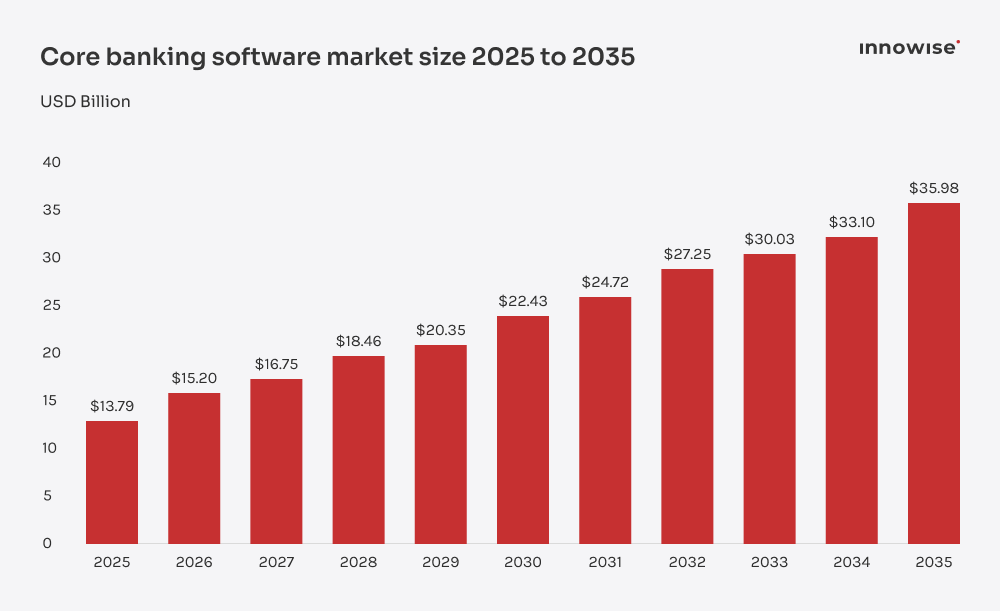

The global core banking software market was valued at $13.79B in 2025 and is projected to grow from $15.20B in 2026 to nearly $36B by 2035, with a CAGR of 10.07%. Growth is being driven by increased fintech investment, rising demand for digital banking services, and stronger pressure on banks to modernize customer experience without adding more cost and complexity.

Now, the obvious question: why not build a core from scratch?

For some banks, that may be an option. But it’s rarely the fastest or safest one. Building a core means owning ledger design, transaction rules, audit trails, security controls, product configuration, reporting, integrations, testing, upgrades, and years of maintenance. It’s a permanent banking infrastructure program.

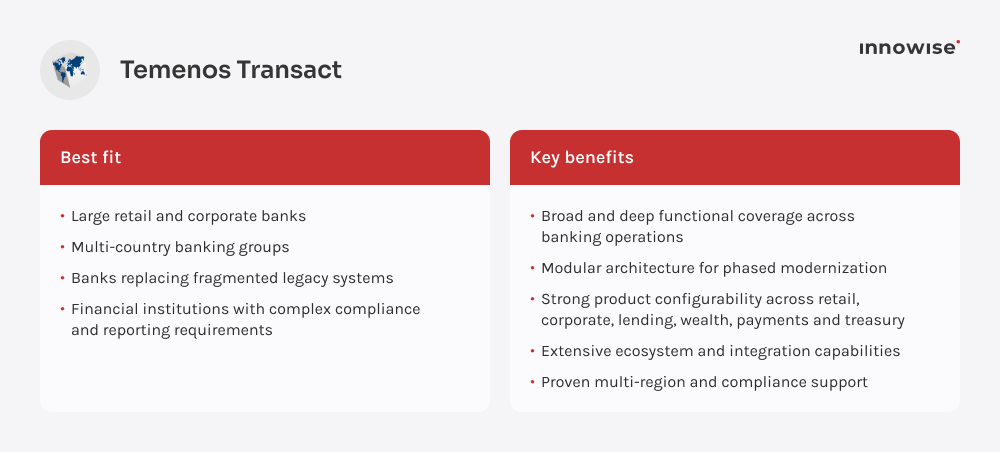

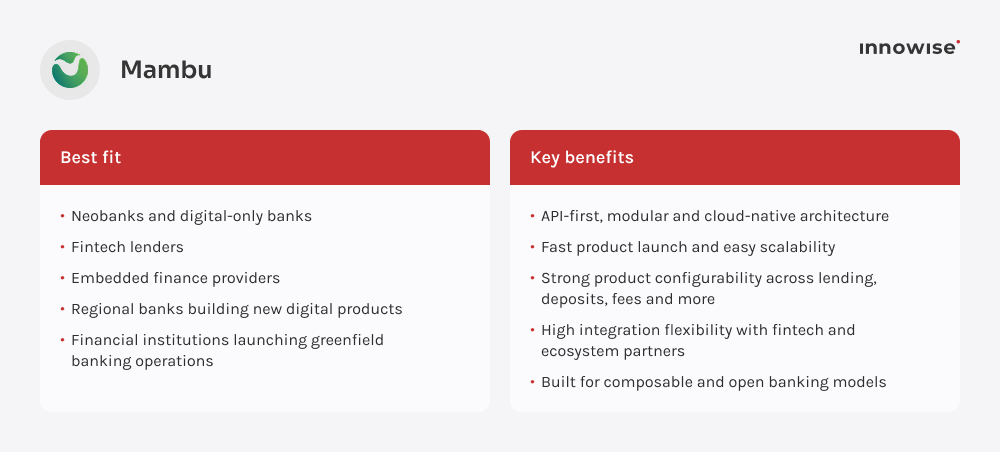

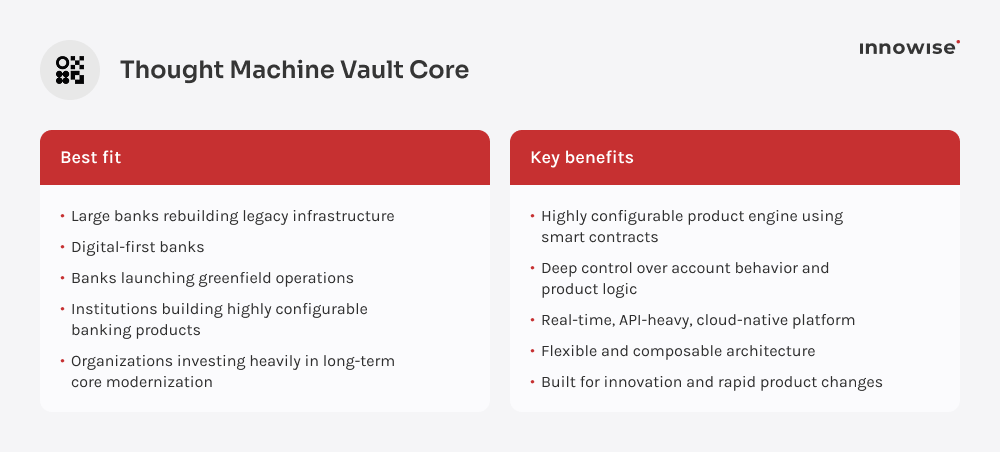

A vendor platform gives you a ready base: account management, ledger operations, transaction processing, product setup, reporting tools, and standard integration options. That cuts a lot of technical risk from day one.

But here comes the part many teams underestimate: the platform still has to fit the bank. It won’t clean your legacy data, map your old loan products, connect every payment provider, or decide how approval flows should work across branches, regions, and business lines. That part requires involvement from subject matter experts (SMEs) and solution architects (SAs) who understand both the software and the business logic behind it.

Companies like Innowise help banks with that layer: adapting core banking systems, building missing modules, connecting third-party services, moving data, and making the new setup work inside the bank’s actual tech stack.

So, in plain terms, a good core banking platform gives you the foundation. A good implementation partner makes sure that the foundation actually supports the business you’re trying to build.

Hire us

Hire us