Hire us

Hire us

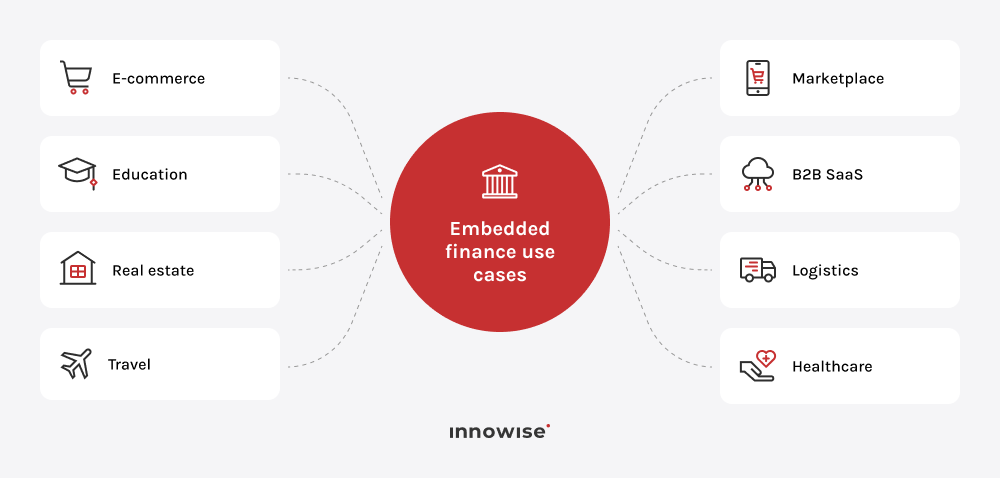

A few factors are converging simultaneously. API-based financial infrastructure has made it technically far simpler for non-financial platforms to offer financial products. Regulatory frameworks in many markets now support this without requiring platforms to become licensed banks. And user expectations have also shifted. People expect financial services where they already spend their time, not as a separate errand. The business case reinforces this: embedded financial products improve retention, generate new revenue, and increase the overall value a platform delivers to its users.

Thank you!

Your message has been sent.

We’ll process your request and contact you back as soon as possible.