Hire us

Hire us

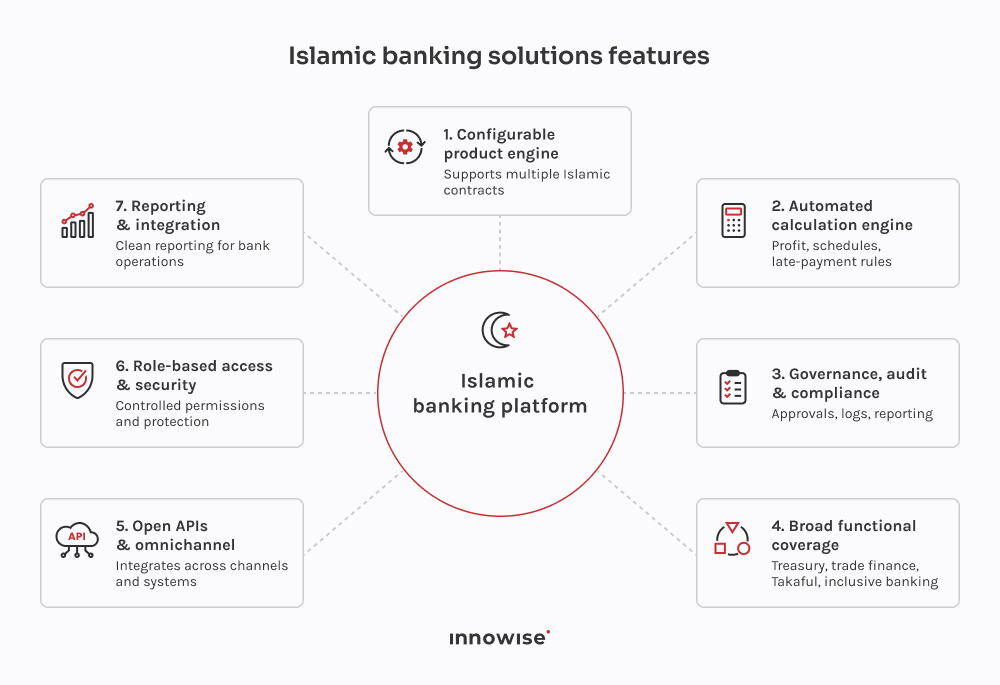

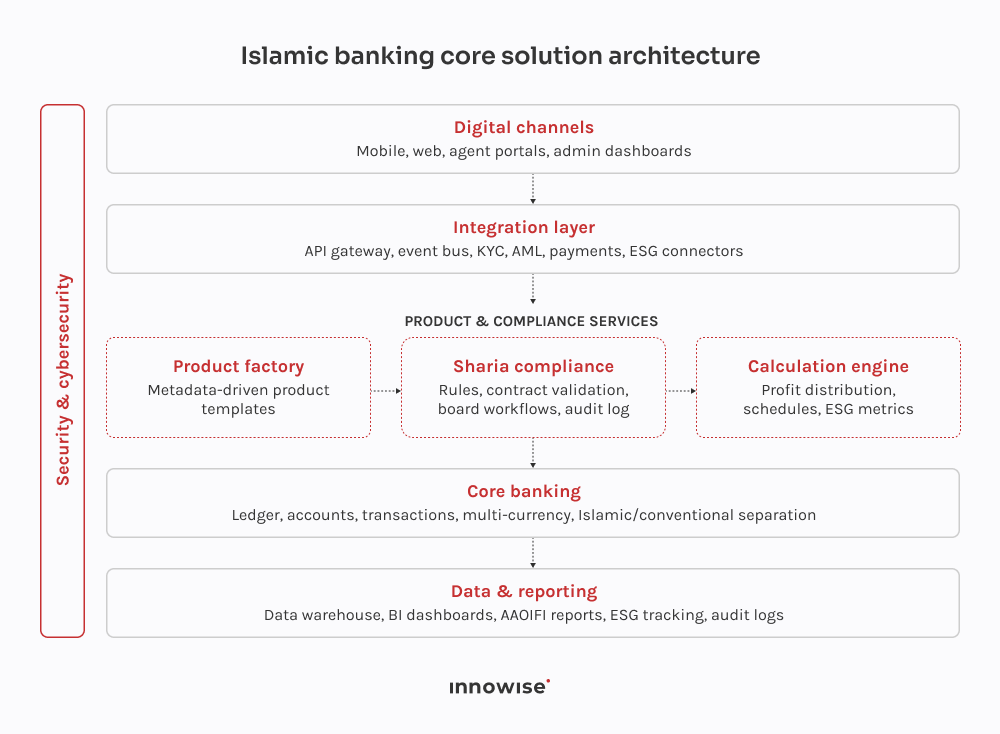

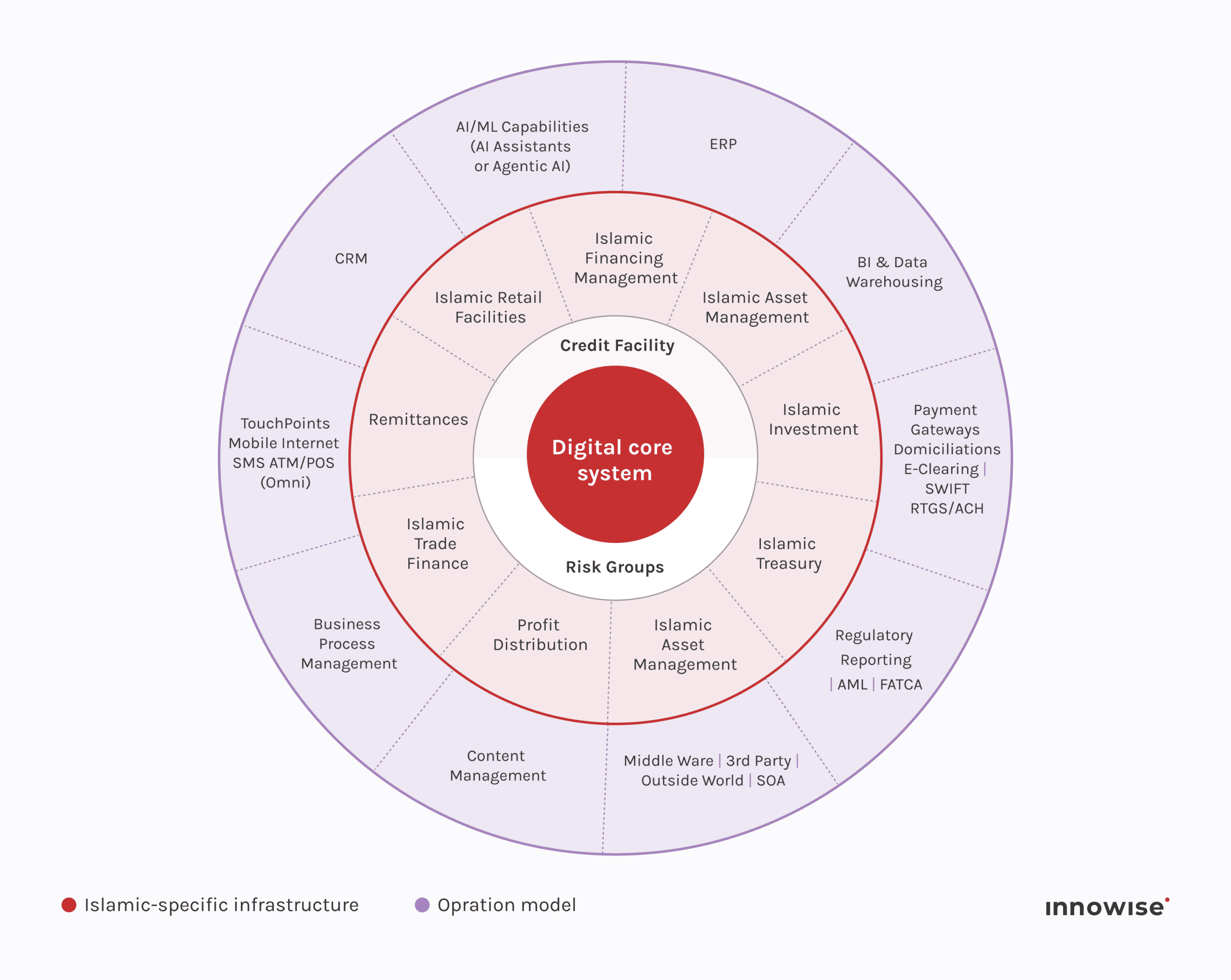

Islamic banking software is a specialized system that manages Sharia-compliant financial products. It's built around contract-based structures like trade, leasing, partnership, and investment, with embedded compliance validation at every step.

Thank you!

Your message has been sent.

We’ll process your request and contact you back as soon as possible.