Thank you!

Your message has been sent.

We’ll process your request and contact you back as soon as possible.

The form has been successfully submitted.

Please find further information in your mailbox.

Modern technology has made transferring money much easier – now, shopping globally is a matter of a couple of button-taps.

And it’s not just FinTech startups and eCommerce platforms that offer more convenient experiences. Legacy banks are also seeking ways to transform the landscape of monetary transactions, simplifying and revolutionizing how we handle money.

But the field is not without its challenges. So today, we break it all down – the mechanisms, challenges, and innovations that shape P2P transactions worldwide today.

Before we talk about more complex ideas, let’s see how P2P transactions work. Contrary to the logical belief, it’s more complicated than just taking money from one bank account and placing it into the other.

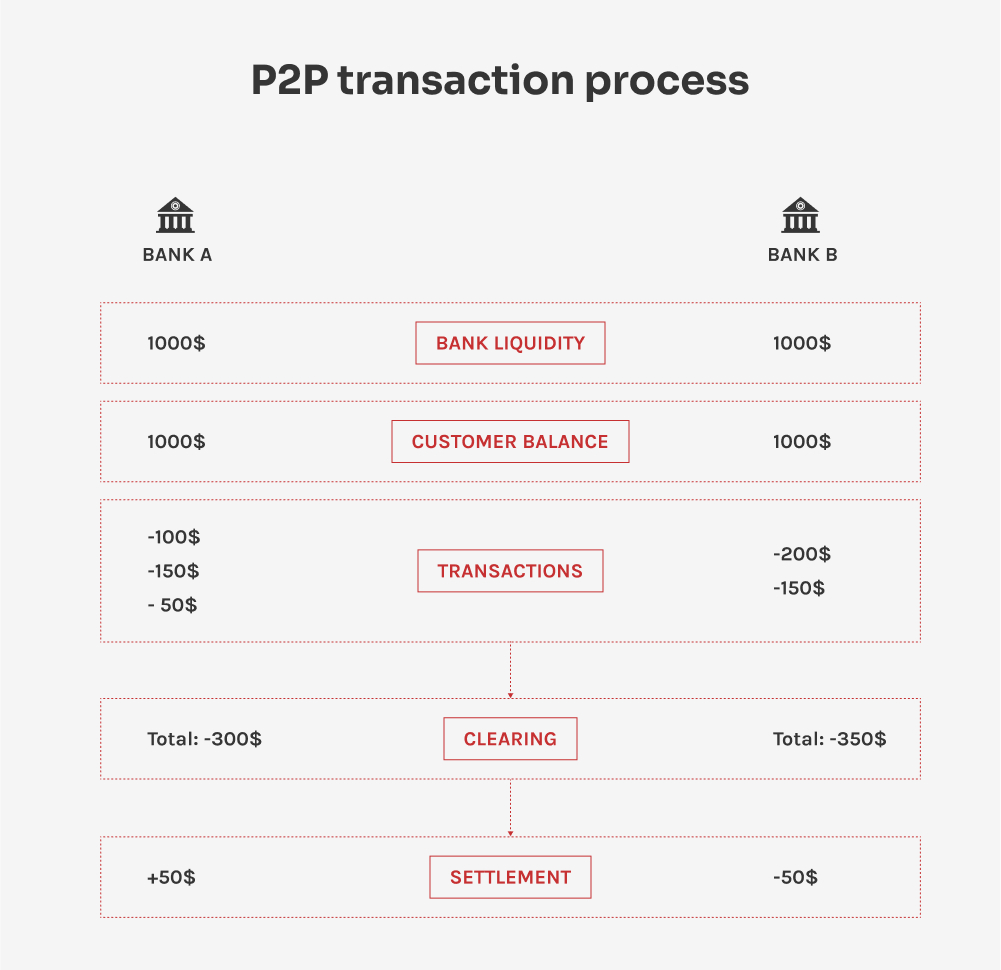

P2P, or peer-to-peer transactions, represent a direct exchange of funds between individuals (peers), bypassing traditional financial intermediaries. The process includes two parts: clearing and settlement, which help to keep clear records of transactions and accurately transfer funds from countless transactions happening throughout the day.

Clearing is the process of validating transactions’ details, which includes identity verification, liquidity checks, and data aggregation. Since the banks handle many transactions throughout any period of time, most of them are consolidated into a single amount during the clearing process. Let’s break it down in more detail:

Having all the required information, the banks can exchange funds. That process is called settlement, where the banks use aggregated transaction data through a set period and just exchange the difference of those transactions. It happens through several stages:

The exchange of information between banks and other financial institutions is facilitated by the advanced technological infrastructure. Many big organizations use SWIFT – The Society for Worldwide Interbank Financial Telecommunication – to deliver transaction reports in a secure and standardized manner.

However, various countries have developed their own systems for P2P transactions, reflecting unique market demands and regulatory environments. For example, the UPI system in India allows instant P2P transfers via mobile platforms.

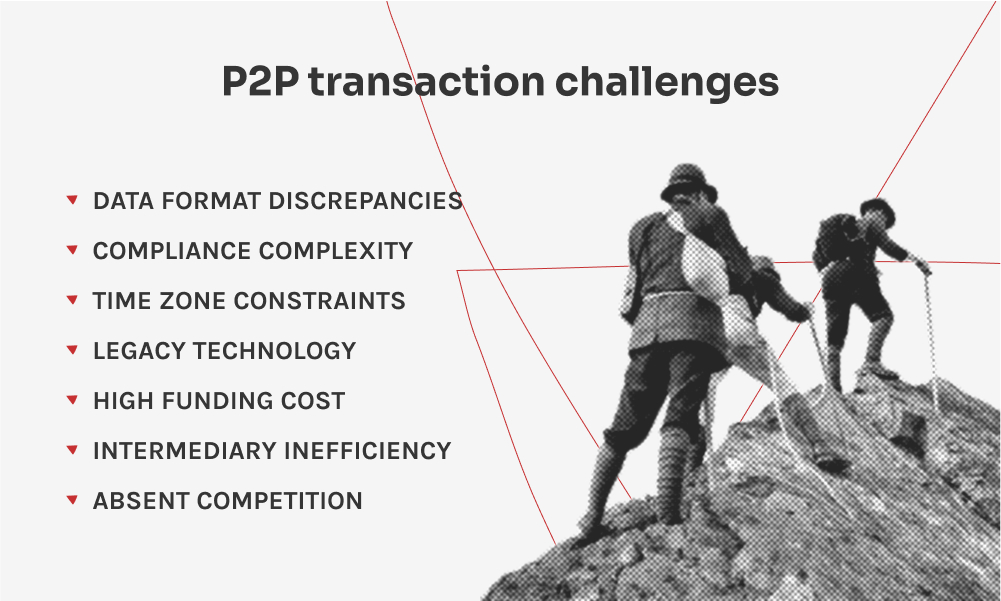

As we can see, clearing and settlement include a lot of information flowing between the actors. The complex nature of those processes is where many issues of P2P transactions stem from.

International P2P transactions face numerous hiccups due to complex global financial infrastructures. The differences in technology and security standards of financial institutions across the globe contribute to transaction issues, increasing the time it takes for the funds to get to the recipient’s account and adding to the workload for finance professionals. Here’s a more detailed breakdown of the prominent P2P transaction challenges:

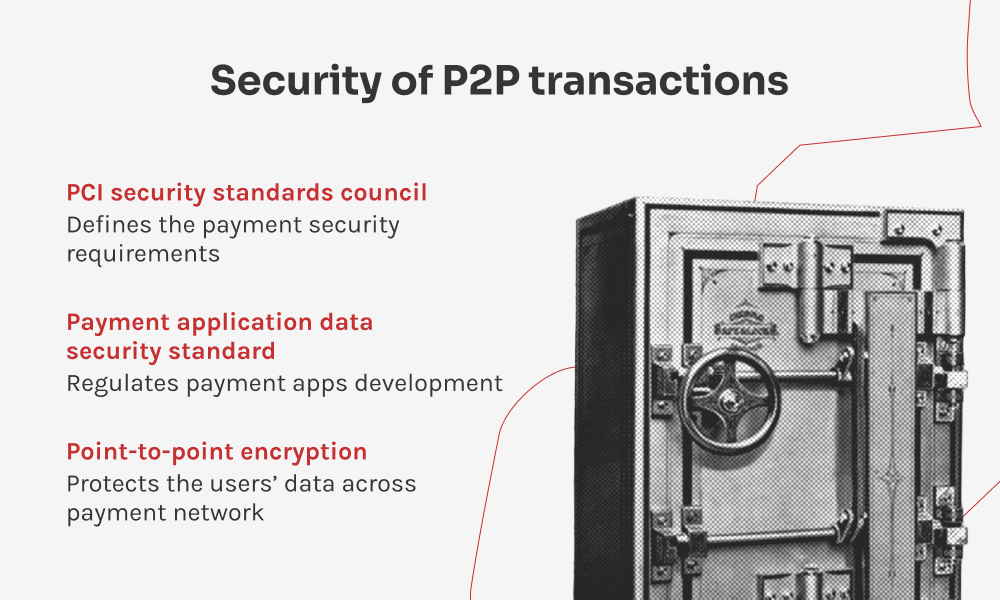

Overall, one of the main benefits of P2PE for merchants is that it significantly reduces the scope of their PCI DSS compliance. Since the cardholder data is encrypted and never exposed in their systems, they have fewer requirements to meet for a secure payment environment.

The evolution of P2P transactions has given users various ways to transmit funds. Each method can boast its own set of features, use cases, and conveniences, but it also comes with distinct security considerations.

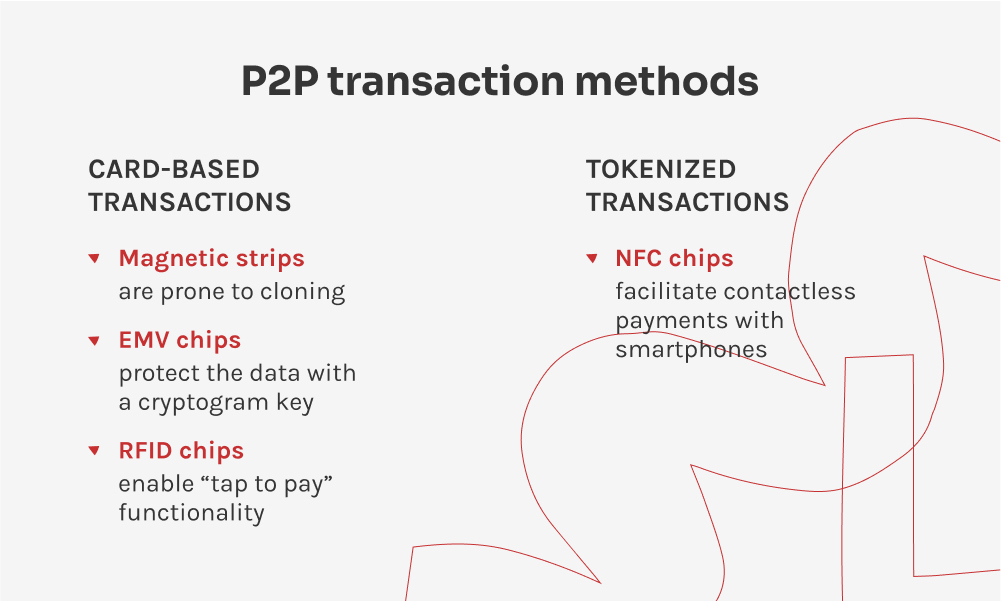

Cards are among the most convenient cashless payment methods. As they continued to evolve, the ways of storing and transmitting cardholder data across merchant networks also changed, intending to strengthen payment security. The payment cards store the data on three carriers: magnetic strip, EMV chip, and RFID chip.

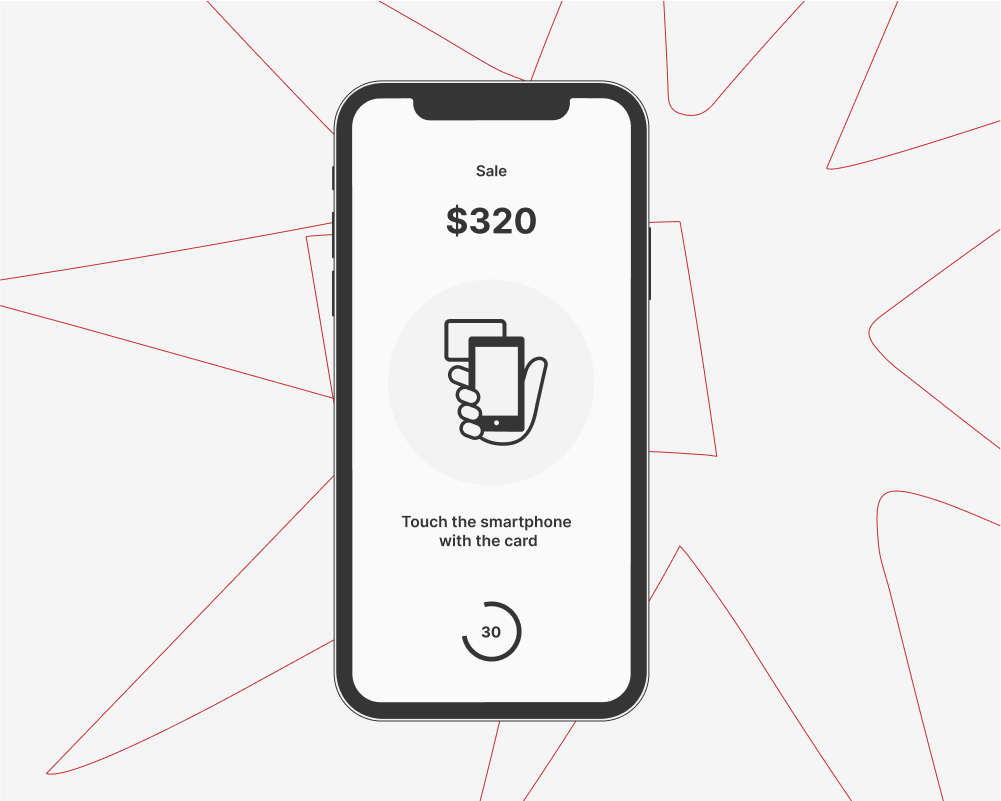

With smartphones becoming the primary computing devices for a significant part of the world, FinTech vendors are looking for ways to make handling one’s finances even more seamless. Online banking is already a given for many people, but with certain technologies becoming more accessible, the world of P2P transactions is also catching up.

Modern smartphones and wearables from almost any budget come with an NFC (Near Field Communication) chip built into the motherboard. It enables data transmission in close vicinity between devices, just like RFID chips that you find on debit and credit cards. The hardware paved the way for the adoption of tokenized transactions, and now users can do away with their cards completely and pay for things by just tapping the POS terminal with their smartphone or watch.

Among the most popular tokenized payment systems are Apple Pay and Google Pay. However, many regional FinTech companies and banks offer their solutions primarily on Android, as it doesn’t restrict access to NFC for third-party applications. With tokenized transactions, users create a clone of their credit card stored on their phone or wearable. Each transaction is assigned a unique, encrypted token, ensuring that actual card details are not shared with the merchant.

There is also the other end of peer-to-peer transactions to talk about. Point of Sale (POS) technology has seen significant technological innovations in recent years: hardware POS systems developed to support a growing variety of payment options, and Contactless Payments on COTS (Commercial Off-The-Shelf) solutions, also known as CPoC, emerged as an alternative. These innovations have transformed the way businesses conduct transactions and interact with customers.

Hardware POSs are separate devices meant to receive and validate transaction information. Over the years, they have acquired several hardware components that allow them to receive payments from multiple sources: strip readers to interact with magnetic strips, EMV readers to recognize EMV chips, and NFC chips to receive tokenized transactions from smartphones and wearables. The downside of hardware POSs is the cost of the entire system: it ranges from $20 up to $1000 for an individual device and from $260 to $3400 for the device kit. In addition, the software that runs the whole thing must also be purchased for upwards of $400.

CPoC solutions are software-based POS systems that offer cost-effectiveness but vary in security and compliance needs. The concept includes using a separate device, like a tablet or a phone, with dedicated software installed that processes transactions. An NFC chip is utilized to read tokenized transactions, while credit card payments require a separate card reader that attaches to the device.

Software-based POSs are easily integrable so that retailers can build their payment ecosystem with contactless payment capabilities at a lower up-front cost. They can also benefit from vast customization options and support for on-the-go payments.

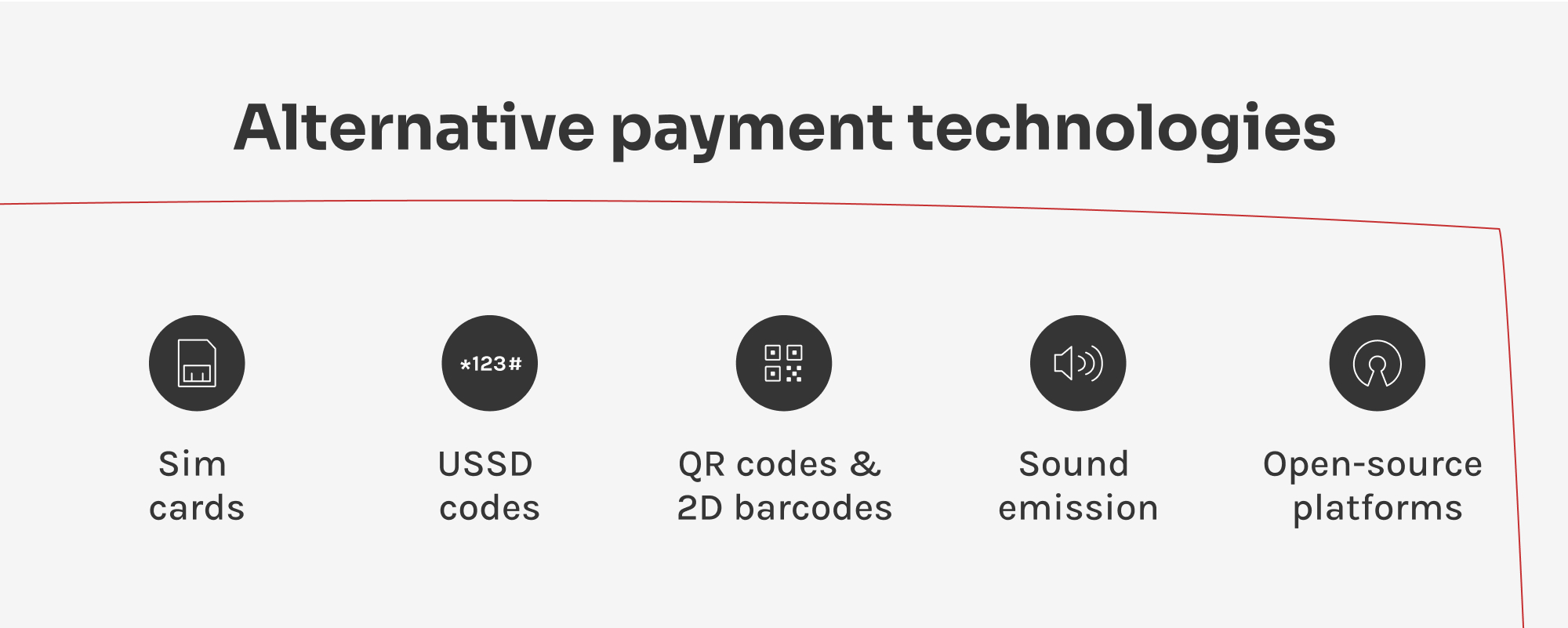

FinTech vendors also developed alternative payment methods for users’ diverse needs and preferences. These methods offer innovative ways to conduct transactions, leveraging technology to make payments more convenient and accessible.

In some regions, mobile phones use SIM cards as virtual EMV chips for transactions. Users can load their payment card details onto the SIM card and make contactless payments by tapping their smartphones on compatible POS terminals.

USSD (Unstructured Supplementary Service Data) is a protocol that allows users to access services through text-based menus on their mobile phones. Users can initiate payments, check balances, and perform other financial operations by sending USSD codes. The method enables transactions without an internet connection, which is crucial in less connected areas.

QR codes and barcodes are widely used for payments in many Asian countries. Customers scan the code displayed by the merchant using their mobile banking apps or other payment apps to initiate transactions. It is a more accessible alternative to tokenized transactions: while they require an NFC chip to initiate a transaction, which many smartphones might not have, you only need a camera to scan the QR code. Using QR codes and barcodes, payment software providers cover a larger user base.

Sound-based payment methods use ultrasonic or audible sounds emitted by devices to transmit payment information. Users can make payments by placing their smartphones near the emitting device. This emerging technology is useful in areas with low smartphone penetration.

Open-source platforms, like Mifos-based payment hub, are engineered to empower organizations to quickly set up and manage their financial operations, providing customers with streamlined P2P transaction experience. Unlike traditional financial systems, which often involve lengthy and complex integration processes, open-source platforms can be implemented quickly. Relying on community-developed software, organizations can avoid the hefty fees of proprietary systems.

Peer-to-peer transactions continue to evolve to stay relevant in the dynamic field of consumer-oriented finance. From SWIFT-based international transfers to innovative FinTech solutions, the methods continue to adapt to offer customers convenient ways to pay and exchange money.

On the other end, the finance world has made significant investments in its infrastructure to prevent fraud. Continuous education, the establishment of up-to-date security standards, and technology like encryption have made leaps in securing customers’ funds. Still, staying on top of emerging vulnerabilities in this arms race is paramount to a safe financial environment. As the technology moves forward, the continued evolution of financial systems will make P2P transactions and financial services more accessible, secure, and efficient.

P2P transactions have transitioned from direct funds exchanges to digitally facilitated transfers. The advent of technology has enabled instant, global transactions without the need for traditional banking intermediaries. Innovations like blockchain and mobile payment apps have further streamlined the process, making P2P transactions more secure, efficient, and accessible to a broader audience.

The PCI Security Standards Council plays a critical role in enhancing cardholder data security across the globe. It develops and enforces standards, such as the PCI DSS (Payment Card Industry Data Security Standard), so that all entities that process, store, or transmit credit card information maintain a secure environment.

The future P2P transaction trends likely to shape this evolution include increased use of blockchain technology for enhanced security and transparency, greater integration of AI and machine learning for fraud detection, and the expansion of mobile payment solutions. Additionally, the rise of digital and central bank digital currencies (CBDCs) may offer new avenues for P2P transactions, further reducing dependency on traditional banking systems.

To stay secure while engaging in P2P transactions, consumers and businesses should prioritize using trusted platforms that implement robust security measures, such as encryption and two-factor authentication. Regularly updating software, being on the lookout for phishing attacks, and using strong passwords are also crucial practices. Additionally, it’s essential for businesses and software developers to be informed about the latest security recommendations provided by the PCI Security Standards Council.

Chief Delivery Officer & Head of Competence Center

Siarhei specializes in navigating high-stakes regulatory environments and complex delivery hurdles. He transforms abstract business requirements into secure, scalable architectures, ensuring that every project is technically sound and future-proofed against market shifts.

Rate this article:

4.8/5 (45 reviews)

Your message has been sent.

We’ll process your request and contact you back as soon as possible.