Please leave your contacts, we will send you our overview by email

I consent to process my personal data in order to send personalized marketing materials in accordance with the Privacy Policy. By confirming the submission, you agree to receive marketing materials

Thank you!

The form has been successfully submitted. Please find further information in your mailbox.

From banking platforms to crypto exchanges, we build high-performance finance software that powers critical operations, manages risk, and supports growth 24/7.

From banking platforms to crypto exchanges, we build high-performance finance software that powers critical operations, manages risk, and supports growth 24/7.

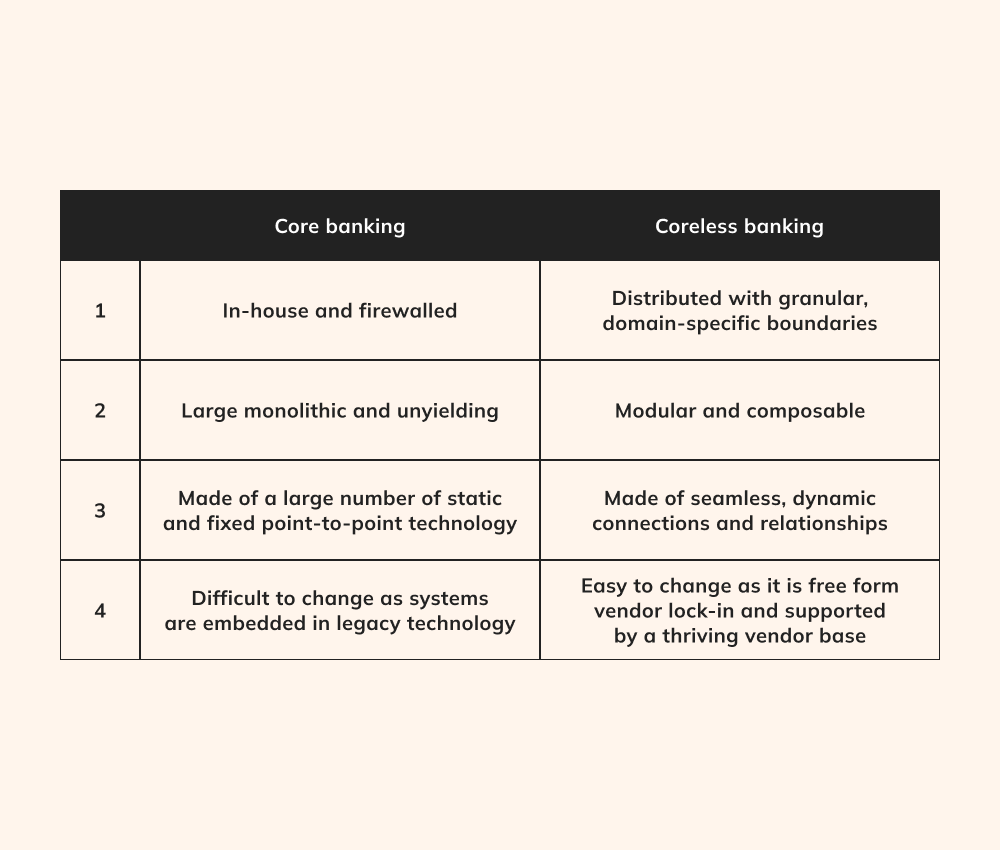

For many years, financial institutions have operated using core banking systems (CBS) to oversee a wide array of crucial operations, like customer accounts, transactions, and payments. However, the time of expansive, all-encompassing core systems that handle everything from recipient details to compliance reporting is currently undergoing a significant change, paving the way for an entirely new perspective — a ‘minimalist’ stance towards the architecture of coreless banking software solutions.

Global Publicis Sapient Banking Benchmark Study engaged 1,000 key figures in senior banking roles and found that ubiquitous acceptance of coreless banking is pivotal in pursuing banking transformation and attaining operational excellence. Thus, 37% of respondents underscored the paramount importance of migrating towards a contemporary, cloud-centric CBS.

What is coreless banking?

Distinct from their counterparts in the financial realm, banking establishments have gained recognition for their heavy dependence on expansive, decades-old software frameworks. These operational systems, while functional, grapple with the challenges tied to rigid, monolithic application architectures. Although innovative design methodologies like serverless computing are widely available, many are reluctant to explore new architectural paradigms due to the threat of security breaches and data loss.

The answer lies in coreless banking, which combines forward-thinking strategies like microservices and APIs to provide the financial sector with adaptable and streamlined software solutions. Despite its infancy, this concept has considerable potential in enhancing tightly interconnected, centralized banking systems while maintaining dependability and security.

Through coreless architecture, developers can initiate discrete updates or deployments, maintaining the independence of application services, elements, or functions. Additionally, this approach mitigates the risk of a single component failure impacting the entire application suite. By liberating financial institutions from legacy infrastructure and conventional development models, coreless banking solutions unlock untapped realms of scalability, efficiency, and cost-effectiveness. Within today’s banking structure, characterized by its ‘coreless’ design, all other components reside beyond this streamlined core, establishing connections through APIs.

Feel like your legacy infrastructure can’t keep up?

Reshape your bank’s software framework with coreless banking solutions.

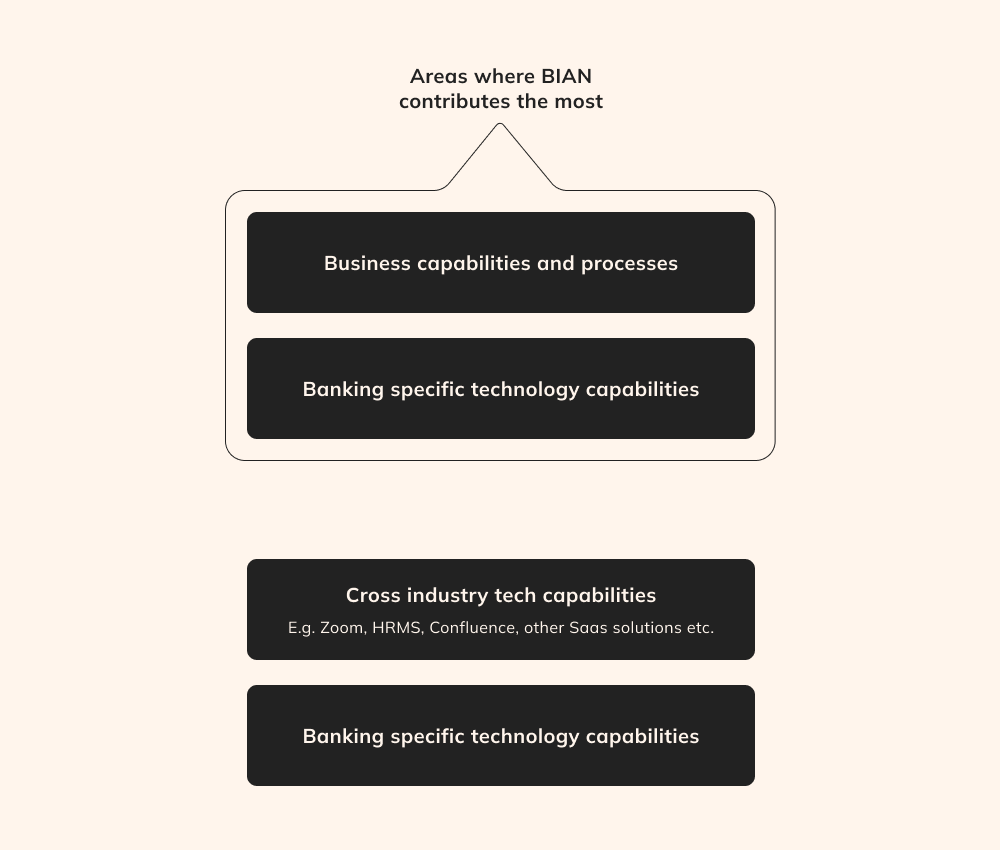

Despite coreless banking’s numerous benefits, its implementation can pose intricate challenges, requiring a reasonable level of standardization to eliminate the slightest chance of failure. This is where the Banking Industry Architecture Network (BIAN) framework comes into play.

As a non-profit consortium of banking entities, technology providers, consultants, and academics worldwide, BIAN provides a framework for addressing concerns about banking interoperability and legacy software. This framework allows the complex and obsolete landscape of core banking architecture to be standardized and streamlined. Based on the principles of service-oriented architecture, it offers banks future-proof methodologies and cultivates an environment of industry-wide collaboration.

From a technological perspective, BIAN proves invaluable by creating digital standards and best practices in service-oriented architecture (SOA) and APIs, equipping banks with detailed tools and guidelines, and ensuring seamless interoperability within banking ecosystems.

As a fundamental underpinning for coreless banking, BIAN eliminates the need to invest time and resources in upholding the foundational “core” of banking systems. Through this strategic move, banks can develop new services and products specifically tailored to their customers’ needs.

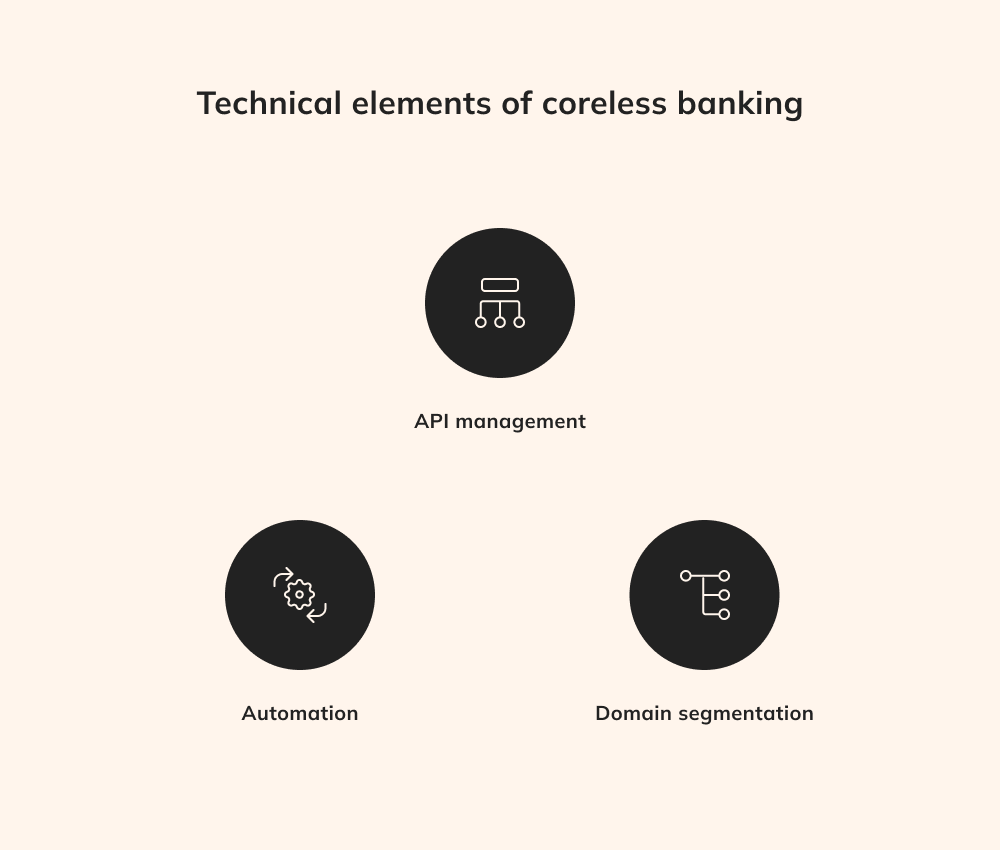

Technical elements of coreless banking

Naturally, the successful establishment of full-fledged coreless banking solutions necessitates more than just the incorporation of microservices, requiring robust API management, systematic automation, and domain segmentation.

API management

In distributed services, APIs’ pivotal role in fostering data exchange and facilitating communication cannot be overstated. Developers should meticulously orchestrate APIs to provide not only data exchange but also robust security measures to safeguard delicate financial transactions. For instance, API management is crucial for executing critical functions, such as approving transactions or maintaining audit trails. This orchestration implies that transactions can be handled appropriately at the API tier, eliminating the need for replication within each discrete app and streamlining the development process.

Automation

A comprehensive embrace of automation is essential for coreless banking software solutions to achieve optimal operational performance and unwavering dependability without time-consuming manual effort. A defining advantage of total automation is frictionless scalability, which adds or removes microservices on demand without downtime. Additionally, automation incorporates application delivery pipelines, allowing developers to roll out novel features quickly, ultimately strengthening the coreless banking potential.

Domain segmentation

Domain segmentation in coreless banking solutions involves dividing the traditional monolithic banking system into distinct functional domains, with each focusing on specific tasks like payments, lending, or customer data. This independence enables more efficient updates since changes made to one domain don’t require changes across the entire system. The segmented architecture enhances flexibility, allowing banks to respond promptly to changing market dynamics, regulatory updates, and customer demands. With domain segmentation, banks can allocate resources to innovate and optimize specific aspects of their services, promoting quicker iteration cycles and encouraging innovation at a granular level without overhauling the entire infrastructure.

Can’t respond quickly to changing market dynamics and customer demands?

Take advantage of enhanced flexibility with a coreless banking ecosystem.

Coreless banking software solutions span many novel technologies, utilizing disruptive capabilities of smart contracts, decentrilized applications, and others to accelerate innovation and transform the customer experience.

Digital identities

Digital identity technologies play a pivotal role in coreless banking by providing secure and verifiable customer identification methods. These technologies, such as biometrics, digital signatures, and two-factor authentication, bolster user authentication and authorization processes, ensuring that only verified individuals can access and manipulate financial services within the coreless ecosystem.

Smart contracts, powered by blockchain, automate and enforce contractual agreements without intermediaries. In coreless banking, smart contracts enable self-executing financial processes, such as automated loan approvals, interest payments, and fund transfers, enhancing operational efficiency, reducing processing times, and minimizing the risk of errors.

Decentralized applications are integral to coreless banking’s modular architecture. DApps run on blockchain networks without central control, offering functionalities like peer-to-peer payments, asset tokenization, and decentralized exchanges. In coreless banking, DApps enhance flexibility and customization, enabling banks to swiftly introduce new services and adapt to changing market demands.

Microservices-based architectures and coreless banking

Microservices-based architectures and coreless banking share a tightly interconnected relationship, working in tandem to revolutionize the financial industry’s operational landscape. Microservices entail breaking down complex applications into smaller, independent components that can be developed, deployed, and scaled individually, with each microservice focusing on a specific task or function.

Coreless banking software solutions disrupt the conventional reliance on fragmented banking transaction compartments. With this concept, every aspect of the bank’s offerings is meticulously categorized as a distinct business function, allowing them to be modified or improved independently, unlike monolithic systems. This modularity enhances flexibility, allowing rapid adaptation to market changes and modern trends. Moreover, microservices can be scaled independently, ensuring optimal resource allocation and handling varying transaction volumes as well as user demands based on specific needs.

In essence, microservices-based architectures complement and enhance coreless banking principles. By embracing microservices, banks can seamlessly implement the coreless approach, redefining how financial services are developed, delivered, and experienced in a more agile, secure, and customer-focused manner.

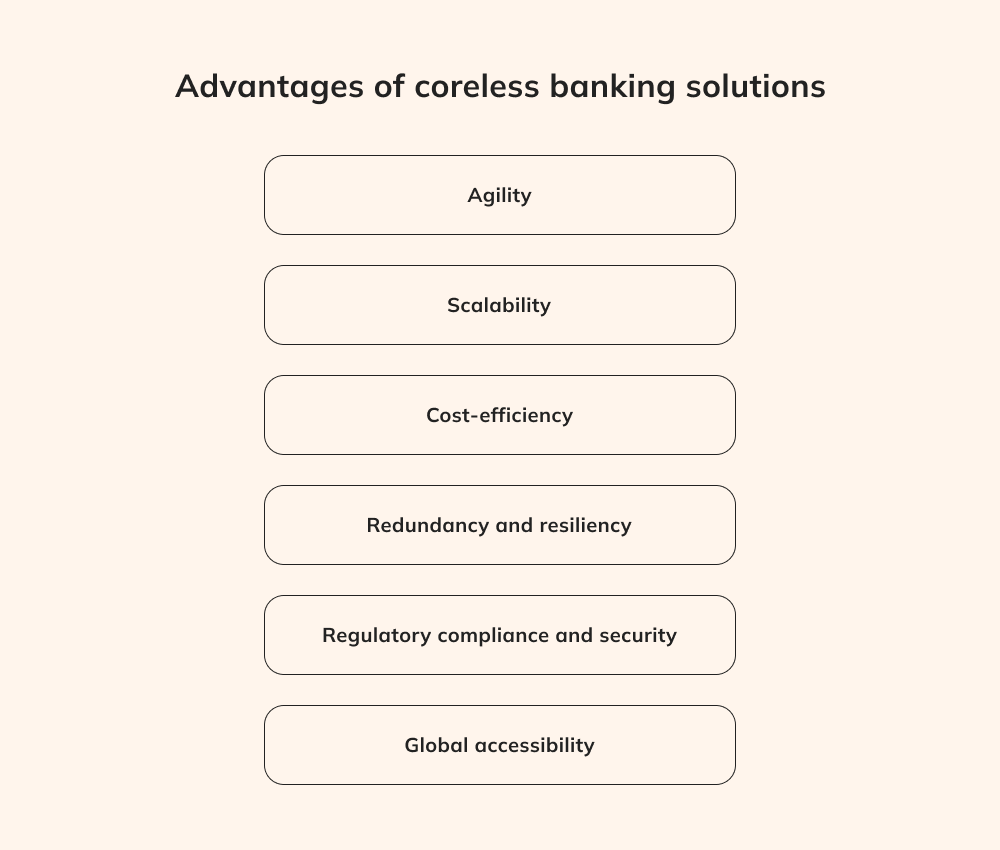

Advantages of coreless banking solutions

Embracing a shift from the traditional monolithic systems, coreless banking solutions offer a multitude of advantages that have the potential to reshape the fintech industry.

Agility

Coreless banking’s agility and flexibility reshape how financial institutions operate. Banks can innovate swiftly through modular microservices, enabling them to introduce new products, services, and features without overhauling their entire infrastructure. As an example, when a bank launches a new mobile payment solution, a microservice can be created to handle digital transactions, providing a seamless user experience while maintaining the integrity of the overall banking platform at the same time.

Scalability

Scalability is a hallmark strength of coreless banking, also rooted in its modular architecture. Microservices act as building blocks that can be independently scaled to meet varying transaction needs and user demands. Banks can, for example, instantly allocate additional resources to the payment processing microservice, ensuring they can handle a spike in transactions, like those on Black Friday, without interruptions and sacrificing performance.

Cost-efficiency

The financial advantages of coreless banking software solutions extend to cost efficiency. This approach significantly reduces the need for large-scale system updates and maintenance since banks are not forced to undergo comprehensive, costly overhauls. Instead, they can precisely target enhancements, creating dedicated microservices to address specific needs. For example, when a bank seeks to integrate a new payment gateway, coreless banking simplifies this process by creating a modular ecosystem, reducing development time and minimizing associated costs.

Open banking

Coreless banking aligns seamlessly with open banking principles, unlocking a realm of collaborative possibilities. By employing well-managed APIs, banks can establish secure connections with third-party fintech providers, enhancing the range of financial services available to customers. For instance, a customer could seamlessly link their bank account with a budgeting app or investment platform through APIs, accessing a comprehensive suite of financial tools. This symbiotic relationship between coreless banking and open banking enriches customer experiences while maintaining the robust security inherent in the coreless ecosystem.

Redundancy and resiliency

The essence of coreless banking lies in decentralization, and this principle yields tangible benefits. The autonomy granted to each microservice ensures that a failure in one component doesn’t affect the entire system. If a hiccup occurs in the account verification microservice, however, due to coreless banking, this issue will not disrupt critical functions like fund transfers and loan processing, bolstering the system’s stability and resiliency.

Regulatory compliance and security

Coreless banking’s meticulous approach to regulatory compliance and security revolves around tailored control since each microservice is equipped to enforce specific security measures. Consider a microservice that handles sensitive customer data. Coreless banking solutions allow microservices to adhere to strict data protection regulations, significantly minimizing the risk of breaches and ensuring unwavering compliance.

Global accessibility

The coreless banking model goes beyond geographical barriers, ensuring global accessibility to financial services. By harnessing digital channels and APIs, customers can access banking services from any corner of the world around the clock. This benefit holds immense value for international businesses, who can seamlessly manage their accounts, initiate transactions, and avail themselves of financial services without the limitations of physical boundaries or time zones.

Challenges with coreless banking

The concept of coreless banking promises to revolutionize the landscape of financial service applications by liberating banks from the constraints of traditional infrastructure. Nevertheless, despite its innovation potential, coreless banking comes with significant challenges and potential drawbacks that require thoughtful consideration.

Integration with legacy systems

Traditional banking systems are characterized by their extensive, intricate structures developed in obsolete languages such as Fortran or COBOL, which might appear foreign to contemporary developers. Moreover, the banking software landscape has conventionally relied on CQRS to distinguish between read and write operations, mitigating the risks of accidental data changes. However, the evolving realm of modern microservices architectures and APIs doesn’t always prioritize CQRS paradigms, adopting more modern software technologies. Therefore, developers embracing coreless banking must immerse themselves in out-of-date Fortran, COBOL, and CQRS, mastering these time-honored languages and patterns to build coreless-driven applications.

Lack of established standards

Coreless banking stands as an evolving conceptual phenomenon rather than a firmly established industry norm. Some players, such as lBIAN, promote tools and strategies to facilitate coreless banking, but the process of reshaping an existing legacy infrastructure into discrete applications remains hazy. With no definitive roadmap for open banking initiatives and no universally accepted standards, organizations are left to explore coreless banking software solutions on their own, determining whether this approach benefits them. Oftentimes, bank software managers find themselves overwhelmed with the demands of day-to-day operations, leaving little room to explore such experimental trends and embrace coreless banking principles.

Alignment with overall business goals

Despite the disruptive potential for increasing operational efficiency and reducing security vulnerabilities, developers who attempt to reshape a bank’s software framework might lack business support due to industry skepticism. Thus, developers should town down their initial experiments with coreless banking by concentrating on lighthouse projects that target low-risk applications. Later, these initiatives can serve as compelling proof of concept when the business sector embarks on revamping legacy systems.

Want to enrich your banking app with a comprehensive suite of financial features?

Leverage coreless banking APIs to unlock a realm of digital services.

Embracing coreless banking allows financial institutions to respond proactively to market dynamics and cater to evolving demands. By adopting this strategic shift, innovative products and services can be developed and deployed quickly.

Undoubtedly, this shift poses formidable challenges – underscoring the existence of organizations like BIAN. In spite of this, the industry is likely to see a wave of exciting innovations once it is aware of the myriad possibilities inherent in a coreless paradigm. Ultimately, this holds the promise of enhancing the industry’s potential to address banking needs in an effective and convenient way.

From core to coreless

In the landscape of modern finance, the concept of coreless banking emerges as a beacon of transformation. It becomes evident that the traditional monolithic banking systems, while once the cornerstone of the industry, now hamper the continuous progress in the field. Coreless banking, with its domain segmentation and modular approach, offers a new path forward by breaking down the rigid structures of the past and embracing a more flexible, agile, and adaptable framework.

In the realm of coreless banking, which is still a revolutionary concept rather than a universally accepted practice, the potential for industry-wide collaboration and innovation is boundless. By adopting this approach, financial institutions can proactively respond to the dynamic market landscape, regulatory changes, and evolving customer expectations. As we bid farewell to the monolithic era, we welcome a future defined by adaptability, innovation, and a renewed commitment to customer-centric financial services in ways that were once considered unattainable.

Chief Delivery Officer & Head of Competence Center

Siarhei specializes in navigating high-stakes regulatory environments and complex delivery hurdles. He transforms abstract business requirements into secure, scalable architectures, ensuring that every project is technically sound and future-proofed against market shifts.