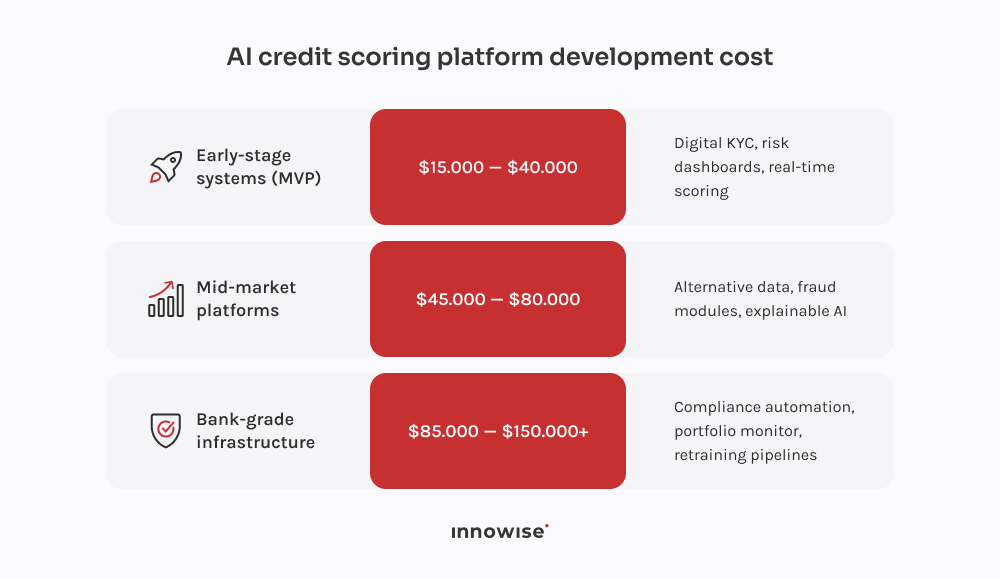

It uses alternative data signals to assess near-term ability to repay, consisting of rent, phone bills & cash flow patterns.

Gracias.

Su mensaje ha sido enviado.

Procesaremos su solicitud y nos pondremos en contacto con usted lo antes posible.

El formulario se ha enviado correctamente.

Encontrará más información en su buzón.

Contrátanos

Contrátanos

Contrátanos

Contrátanos Contrátanos

ContrátanosSeleccionar idioma