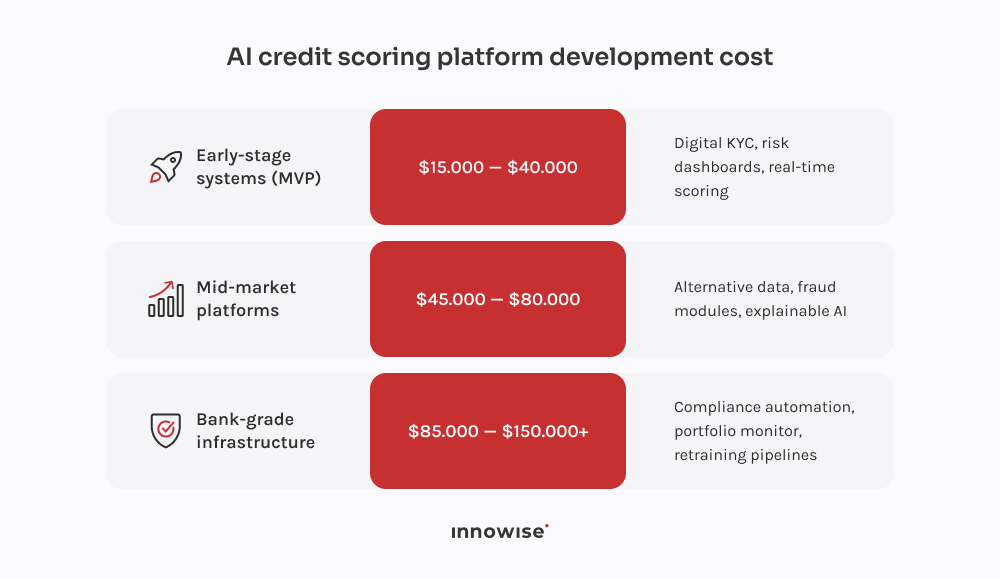

It uses alternative data signals to assess near-term ability to repay, consisting of rent, phone bills & cash flow patterns.

Thank you!

Your message has been sent.

We’ll process your request and contact you back as soon as possible.

The form has been successfully submitted.

Please find further information in your mailbox.

Hire us

Hire us