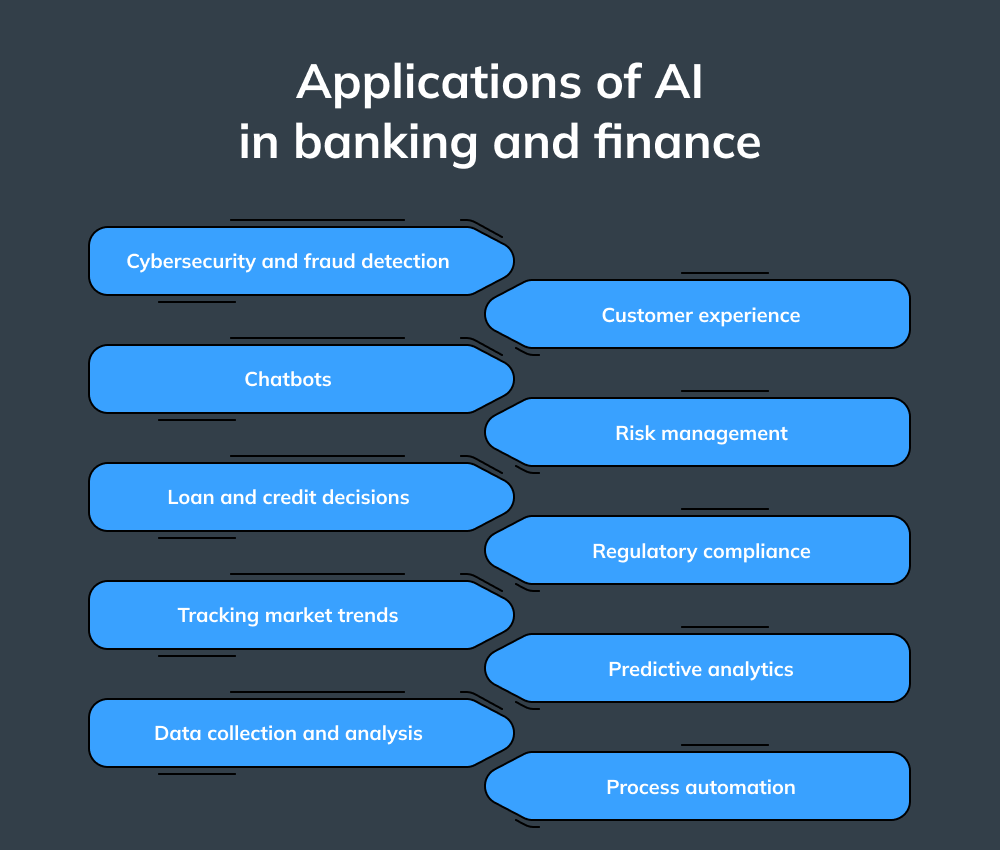

Applications of AI in banking and finance

AI has woven itself into the daily fabric of our lives – transforming industries in ways we could only imagine a few years ago. Denying its importance would be shortsighted: the banking and finance sector in particular has seen huge change thanks to FinTech innovations, bringing a host of benefits to both stakeholders and customers alike.

Cybersecurity and fraud detection

Every day, millions of transactions flow through the banking system: people pay bills, deposit money, withdraw funds, cash checks, and more. Behind the scenes, banks are in a constant race to stay ahead of cybercriminals – ramping up their security efforts to protect operations and assets and to stop fraudulent activities before they even have a chance to happen.AI is now a key player in this high-stakes game. Banks can use the potential of artificial intelligence to improve digital payments, detect software vulnerabilities, identify suspicious customer behavior all while reducing the risk of scams. Machine learning – a subset of AI – helps detect and prevent illegal actions like email phishing, credit card and mobile fraud, identity theft, and fake insurance claims.Take Denmark’s Danske Bank, which recently updated its obsolete fraud detection software with modern AI algorithms. Thanks to ML’s ability to analyze past transactions (think personal information, data, IP address, location, and so on), the bank saw a 50% increase in fraud detection accuracy and a 60% reduction in false positives. As banks are prime targets for hackers, the widespread adoption of ML and AI is crucial. These technologies help financial organizations respond quickly to digital threats, strengthening their defenses against cyberattacks before they compromise internal systems, employees, or customers.Chatbots

Using chatbots in banking is one of the more straightforward examples of AI implementation. Once deployed, they’ll stay available around the clock, unlike human staff with fixed schedules and the need for regular breaks. Chatbots don’t just respond with one-size-fits-all answers to queries: they learn from customer interactions, building up a body of knowledge that lets them predict user needs and tailor their responses accordingly. By integrating AI-powered chatbots into banking apps, managers can be sure that their clients receive personalized customer support 24/7, with products and services customized to individual needs.An example of a successful chatbot can be seen in the form of Erica: an AI-powered virtual assistant from the Bank of America. Since 2019, Erica has handled over 50 million customer requests – from helping clients reduce their credit card debt to updating card security.Loan and credit decisions

Banks today are employing a wide range of intelligent tools to improve the accuracy, precision and profitability of their loan and credit decisions. Conventional banking software often falls short, plagued by errors, inaccuracies in transaction histories, and misclassifications of creditors. Financial organizations need to closely monitor credit histories and client references when extending credit and evaluating the solvency of individuals or companies. AI-based systems analyze customer behavior patterns to make data-driven decisions concerning creditworthiness, promptly alerting banks to any suspicious or risky activities.Customer experience

Customers have come to expect an intuitive, no-fuss user experience when managing their banking apps. Gone are the days when visiting a bank branch was necessary for simple transactions like deposits and withdrawals, thanks to the convenience of ATMs.Nowadays – with a more tech-savvy population – banks need to continuously innovate to provide quick and secure digital payment solutions. AI helps to reduce the time needed to record KYC information and eradicate errors, streamlines fast product time-to-market, and proactively addresses pre-launch issues before they arise.If that wasn’t enough, applying for a personal loan has never been easier. Customers no longer need to go through the hassle of manual applications: AI and ML in FinTech slash approval times, capturing precise and error-free data concerning customer accounts.Risk management

Currency swings, political upheavals, natural disasters, and armed conflicts can all send shockwaves through the financial and banking systems. During turbulent times, making wise investment decisions is crucial to stay afloat and avoid financial losses. This is whereAI comes into play:- by providing a useful overview of current events, forecasting future trends and predicting what lies ahead, AI helps investors navigate uncertain waters with confidence. AI also can help to determine whether or not a client will be able to repay a loan by analyzing behavioral patterns, credit history, and available personal data.Regulatory compliance

FinTech stands out as one of the most heavily regulated sectors in the global economy. Governments play a big role as the primary watchdogs – monitoring and overseeing banks to prevent financial crimes, money laundering, and tax evasion.Legal requirements and standards shift frequently – meaning banks need to maintain well-informed, agile departments dedicated to researching and implementing ever-changing financial legislation. When done manually, this process is both time-consuming and costly. Enter AI: using the power of deep learning and NLP), AI systems can quickly analyze new regulations and assess compliance requirements, making sure organizations meet all external laws as well as internal policies. While AI isn’t a substitute for a skilled human compliance analyst, it can pinpoint critical or ambiguous aspects of regulation and safeguard the company against legislative risks.Predictive analytics

Using AI for predictive analytics is a little like having a highly intuitive assistant that can pinpoint trends and correlations that humans or conventional tech often overlook. AI is widely used in natural language analysis and general-purpose semantics, thanks to its ability to quickly detect specific patterns and data correlations. This is a gamechanger for the banking sector: predictive analytics help financial institutions define untapped sales opportunities, deliver data-driven metrics, and reveal industry-specific insights that can significantly boost revenue.Why should the banking sector embrace AI?

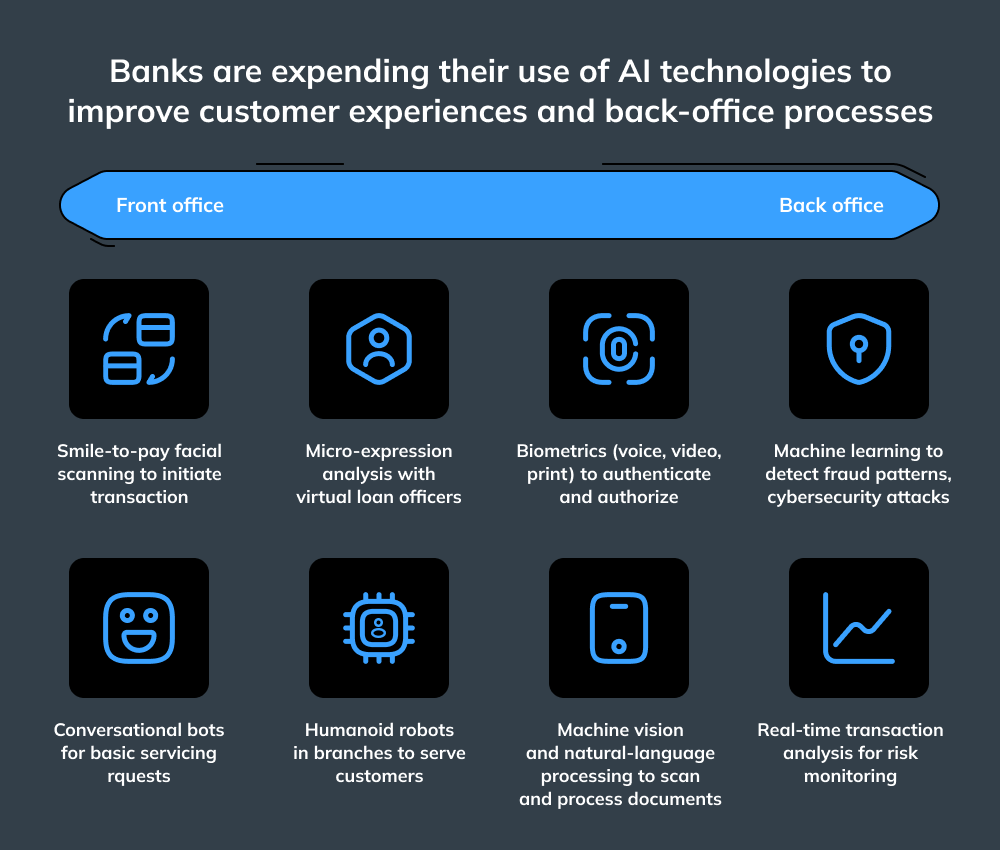

The banking world is shifting rapidly toward customer-centric models that aim to meet every client’s wants, needs, and expectations. Today’s customers want their banks to be available 24/7, offering innovative tools and features that make their banking experience hassle-free. To meet these expectations, banks must first tackle internal challenges, such as legacy software systems, fragmented data silos, limited budgets, and subpar asset quality. Once these obstacles are bypassed, banks are one step closer to embracing AI for their everyday problems.AI doesn’t just ensure unmatched cybersecurity: it also makes financial services more convenient and time-saving for both clients and employees.

Challenges in the wider adoption of AI in finance and banking

It goes without saying that AI comes with a package of countless benefits – but its widespread adoption is hindered by various issues such as credibility gaps and security risks that loom large. A holistic strategy and comprehensive approach to AI and machine learning in finance can significantly decrease these risks, increasing the likelihood of success and the financial gains that come with it. As decision-makers navigate the exciting world of AI in finance, they might encounter a number of common obstacles, outlined as follows.

Data security

AI collects, stores, and handles huge amounts of sensitive personal information – meaning that it’s imperative for financial institutions to establish protection measures to prevent data breaches and unauthorized access. Banks should prioritize ironclad data protection systems when handling large volumes of AI-related information in order to eliminate any risks and to keep confidential information secure.Lack of quality data

Insufficient data quality poses a big challenge for FinTech companies. Without well-organized data, applying insights to real-life situations is close to impossible if it doesn’t correspond to current realities. Additionally, data that differs from the machine-readable format can lead to unpredictable behaviors in AI models.Banks looking to adopt artificial intelligence should modify – and, if necessary, overhaul – their data policies and introduce more order in data flows.Explainability issues

Since AI-based software weeds out mistakes and save time, they are widely employed in decision-making procedures. Unfortunately, they may have biases derived from previous human judgment errors. This can mean that the bank’s reputation might be at risk if minor discrepancies in AI escalate and cause large-scale problems. All data involved in AI scenarios should be clear and transparent, leaving no space at all for potential discrepancies.How Innowise can accelerate your AI journey