Please leave your contacts, we will send you our overview by email

I consent to process my personal data in order to send personalized marketing materials in accordance with the Privacy Policy. By confirming the submission, you agree to receive marketing materials

Thank you!

The form has been successfully submitted. Please find further information in your mailbox.

From banking platforms to crypto exchanges, we build high-performance finance software that powers critical operations, manages risk, and supports growth 24/7.

From banking platforms to crypto exchanges, we build high-performance finance software that powers critical operations, manages risk, and supports growth 24/7.

According to the United Nations Office on Drugs and Crime (UNODC), an estimated 2–5% of the global GDP — about $800 billion to $2 trillion — is laundered every year. That’s a mind-blowing amount of dirty money distorting economies, slowing down development, and breaking trust in the financial system. Now, think about this in real-life terms — imagine how many attempts to launder money happen every single day. Pretty terrifying, right?

That’s where AML transaction monitoring comes in. It’s like having a financial watchdog on duty 24/7, keeping an eye on millions of daily transactions — transfers, deposits, and withdrawals — to sniff out anything suspicious. Think of it as the front line in the battle against financial crime, working in real-time (or pretty close) to catch anything that doesn’t add up.

AML transaction monitoring is a fascinating mix of tech, strategy, and vigilance that’s worth knowing about. Ready to dig into the nuts and bolts of it all? Let’s dive in!

$17.59bn

the estimated value of the AML transaction monitoring global market in 2024

source: Fact.mr

9.4%

projected CAGR of the AML transaction monitoring global market by 2024

source: Fact.mr

The role of AML transaction monitoring

When it comes to fighting financial crime, AML transaction monitoring is here, analyzing every transaction — big or small — to catch anything suspicious. Why is this so important? Because criminals aren’t obvious about their moves. They use all sorts of tricks like smurfing to break large amounts into small, harmless-looking transactions to fly under the radar. AML systems harness ML to identify unusual transaction patterns, AI-driven behavior analysis to pinpoint activities that deviate from a customer’s normal profile, and sophisticated rule-based engines to flag transactions that breach regulatory thresholds.

In addition to traditional financial systems, cryptocurrencies have added a new layer of complexity to AML efforts. Their anonymity and decentralized nature make them a convenient tool for criminals to launder money or fund illegal activities without detection. Traditional AML methods, like customer checks and suspicious activity reporting, struggle to keep up in this space. That’s why effective transaction monitoring with advanced tools like blockchain analysis and monitoring is so important — it helps identify and stop illicit activity, adapting to the shifting dynamics of the digital financial world.

Let Innowise help you tackle fraud and security challenges head-on.

What makes strong AML transaction monitoring systems

AML transaction monitoring is a no-brainer for financial institutions, but here’s the kick — not all systems actually deliver. Just having one doesn’t mean it’s doing what it’s supposed to do or catching what it’s meant to catch. So, what’s the secret sauce that makes a great system? Let’s break it down and uncover what really sets the best ones apart.

Risk mapping

A strong AML transaction monitoring system analyzes transaction patterns, locations, business types, and more to create detailed risk profiles. These profiles help identify potential exposure to financial crime and adjust monitoring based on each customer’s overall risk level.

Rule and scenario flexibility

The system must offer adaptable rule and scenario configurations. It must not only handle standard patterns and requirements but also let you tweak things to stay on top of changing regulations, industry trends, and new fraudulent tactics.

Regulatory integration

With updates to compliance rules, reporting requirements, and risk factors popping up all the time, a solid AML transaction monitoring system needs built-in tools to keep up with these shifts automatically.

Dynamic monitoring

The system should handle both real-time and ongoing monitoring. Real-time keeps you in the loop with instant alerts for suspicious activity, while ongoing monitoring looks at the bigger picture, spotting trends and patterns over time.

Automation and analytics

A solid AML transaction monitoring system has automation and advanced analytics working together. Automation takes care of the monitoring process and generating Suspicious Transaction Reports (STRs), while advanced analytics dives into the data to spot patterns, trends, and red flags.

Smart AI detection

The monitoring system should use advanced AI to sharpen detection and reduce false positives. AI algorithms make monitoring faster and more reliable as they can spot tricky patterns and anomalies that traditional methods might overlook.

Scalability and integration

An AML transaction monitoring system should be built to scale and keep up with growing transaction volumes and complexity. It should also integrate effectively with your existing IT ecosystem for a smooth data flow and process automation.

Red flags for high-risk transactions

Certain indicators almost always classify transactions as high-risk, triggering the AML transaction monitoring process for further scrutiny. Understanding and applying these red flags helps spot the suspicious transactions and make sure nothing slips through the cracks.

Cash-intensive transactions

Cash deposits or withdrawals are hard to trace, and when they involve large amounts, they may signal activities like money laundering, tax evasion, or drug trafficking.

Round-number transactions

Repeated transactions in neat, round amounts often point to structuring or money laundering techniques, as criminals try to move funds without drawing attention.

Dormant account activity

Sudden and unexplained transactions in accounts that have been inactive for a long time may indicate attempts to use them for fraudulent purposes.

High-risk sectors and regions

Transactions linked to industries like gambling or involving regions known for weak financial regulations are often flagged for potential money laundering.

Shells and tax havens

Transactions linked to shell companies, front companies, or tax havens are known for their potential role in hiding the origin of illicit funds or evading taxes.

Unexplained source of funds

Transactions where the origin of funds cannot be verified or are missing required documentation often indicate potential money laundering or other illegal activities.

Related party transactions

Transfers between accounts owned by the same individual or closely related parties can raise red flags, especially if the activity lacks a clear business purpose.

Unusual payment methods

High-value transactions through less common methods, such as virtual currencies, are often flagged because they’re hard to trace and can be tied to shady activities.

AML transaction monitoring process

Now that we’ve covered the basics of solid AML transaction monitoring systems and the red flags to watch for, let’s pull back the curtain and see how it all works. Here’s a step-by-step look at what’s happening behind the scenes.

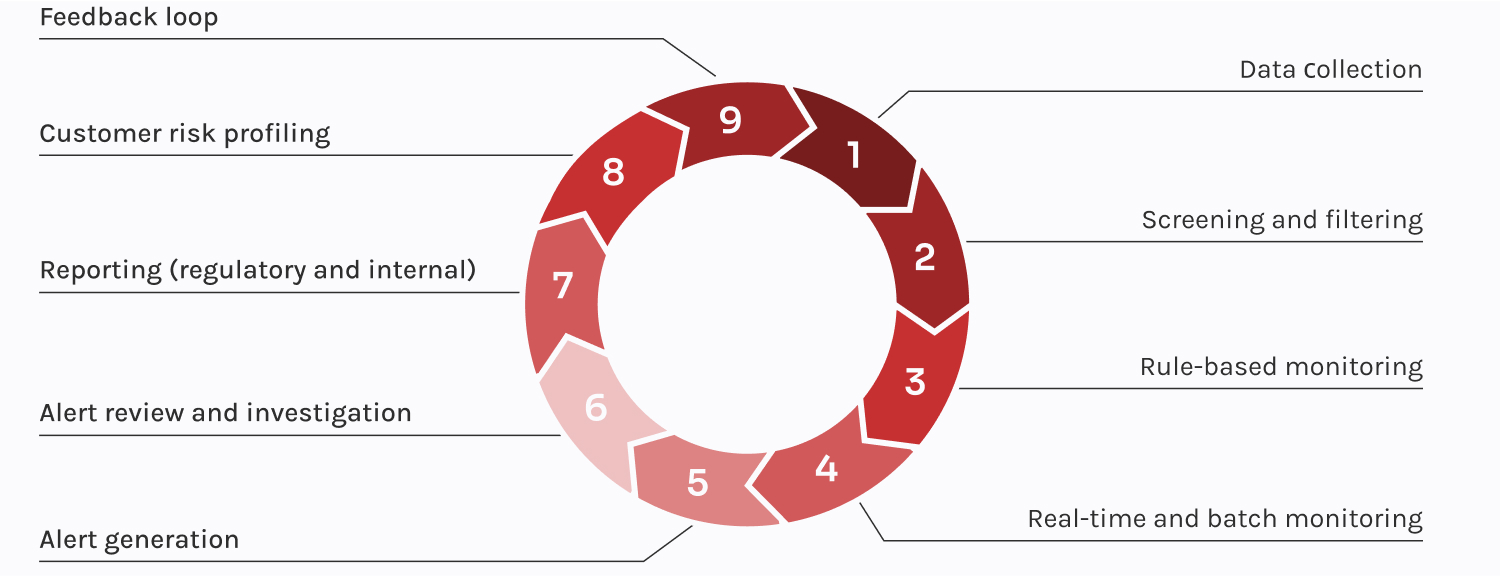

01

Data collection

The system gathers all the essentials: customer information, transaction details, external data from sanctions lists and PEP databases, and historical activity patterns.

02

Screening and filtering

This is where transactions get checked against key regulatory watchlists, sanctions, and PEP databases. It’s all about spotting red flags early and flagging high-risk activities for a closer look.

03

Rule-based monitoring

The system applies predefined rules such as thresholds for large transactions, frequency of small deposits, activity in high-risk regions, or deviations from a customer’s usual behavior.

04

Real-time and batch monitoring

Real-time monitoring catches suspicious activity as it unfolds, while batch monitoring analyzes groups of transactions to spot trends and anomalies over time.

05

Alert generation

When a transaction crosses a set threshold or shows unusual behavior, the system generates an alert that prompts investigators to look at the flagged transaction for further analysis.

06

Alert review and investigation

When an alert pops up, investigators dig into the transaction to figure out if it’s suspicious or a false positive. If it’s a real risk, the case is escalated for further action.

07

Reporting (regulatory and internal)

This stage focuses on creating reports for internal records and regulatory compliance. STRs are filed with authorities, while internal reports track findings and support risk management.

08

Customer risk profiling

Ongoing profiling tracks customer activities and behavior to keep their risk levels up to date and make sure the system stays focused on high-risk customers and adapts as things change.

09

Feedback loop

Feedback from investigations, audits, and regulatory changes is used to update rules, reduce false positives, and improve detection accuracy to stay ahead of new risks and tactics.

01Data collection

The system gathers all the essentials: customer

information, transaction details, external data from sanctions lists and PEP databases, and historical activity

patterns.

02Screening and filtering

This is where transactions get checked against

key regulatory watchlists, sanctions, and PEP databases. It’s all about spotting red flags early and flagging

high-risk activities for a closer look.

03Rule-based monitoring

The system applies predefined rules such as

thresholds for large transactions, frequency of small deposits, activity in high-risk regions, or deviations

from a customer’s usual behavior.

04Real-time and batch monitoring

Real-time monitoring catches suspicious activity

as it unfolds, while batch monitoring analyzes groups of transactions to spot trends and anomalies over time.

05Alert generation

When a transaction crosses a set threshold or

shows unusual behavior, the system generates an alert that prompts investigators to look at the flagged

transaction for further analysis.

06Alert review and investigation

When an alert pops up, investigators dig into

the transaction to figure out if it’s suspicious or a false positive. If it’s a real risk, the case is escalated

for further action.

07Reporting (regulatory and internal)

This stage focuses on creating reports for

internal records and regulatory compliance. STRs are filed with authorities, while internal reports track

findings and support risk management.

08Customer risk profiling

Ongoing profiling tracks customer activities and

behavior to keep their risk levels up to date and make sure the system stays focused on high-risk customers and

adapts as things change.

09Feedback loop

Feedback from investigations, audits, and

regulatory changes is used to update rules, reduce false positives, and improve detection accuracy to stay ahead

of new risks and tactics.

“In today’s business world, the truth is clear: fraudsters grow more sophisticated, and simply following the rules isn’t enough — you’ve got to stay one step ahead. AML transaction monitoring is the shield that helps you catch the unexpected before it turns into a problem. This isn’t about ticking compliance boxes; it’s about building a system that keeps you protected from every angle.”

Dzianis Kryvitski

Delivery Manager in Fintech

Benefits of AML transaction monitoring

AML transaction monitoring is a powerful tool in the fight against financial crime that positively impacts every aspect of a business. Together, its benefits create a stronger, more secure ecosystem that safeguards operations and builds trust.

Regulatory compliance

Businesses need to follow many regulations regarding AML, CTF, and fighting financial fraud. A strong AML transaction monitoring system helps you spot suspicious activity early and file reports on time, preventing penalties, costly audits, and potential restrictions on your business.

Risk mitigation

AML transaction monitoring helps assess exposure to various forms of financial crime and take proactive measures to reduce these risks. This is essential to a broader risk management strategy that helps strengthen your business’s overall financial stability and resilience.

Brand integrity

Trust is vital in financial relationships, and if a business can’t detect suspicious activities, it can quickly lose that trust. AML transaction monitoring helps you build an image of a trusted partner, nurture customer loyalty, and avoid costly reputational consequences.

Operational efficiency

A solid AML transaction monitoring system handles tons of data automatically, cutting down on mistakes and saving you from wasting time on false positives. It lets your team focus on the real threats and prevents considerable resource drain.

Customer protection

AML transaction monitoring helps protect customers from identity theft, unauthorized transactions, and other forms of financial fraud. It creates a safer experience for clients and shows your commitment to safeguarding their financial well-being.

Financial stability

AML transaction monitoring helps keep the bank’s finances stable by flagging high-risk transactions and protecting its capital. It helps prevent cash flow disruptions caused by frozen assets, regulatory fines, or operational delays.

The massive amount of daily transactions makes banks a key target for money laundering. Criminals break up large sums, route funds through complex transfers, or hide illicit money using fake trade deals. AML solutions for banks quickly spot these red flags, ensuring compliance and safeguarding financial integrity.

Money transfer services

With their fast-paced, high-volume transactions and minimal documentation, money transfer services are a magnet for financial crime. AML tools step in to catch irregular patterns, like small, repeated transfers or payments to high-risk regions, flagging them for further investigation.

Wealth and investment management firms

Wealth and investment management firms handle complex portfolios, which makes them targets for financial crime. AML transaction monitoring flags investments linked to high-risk jurisdictions and detects portfolio irregularities to protect client assets and the firm’s reputation.

Lending companies

Loans can be a clever way to launder money — criminals use falsified documents, inflated credit scores, or questionable repayment patterns to funnel illicit funds. AML monitoring helps lenders weed out fake profiles and flag loans tied to high-risk sectors.

Currency exchanges

Currency exchanges are hotbeds for laundering, with criminals using rapid trades to clean dirty money. AML systems track trading patterns, catch suspicious fund movements, and flag accounts trying to dodge detection with small, frequent trades.

Cryptocurrency platforms

Criminals use cryptocurrency platforms for their speed and anonymity, shuffling funds across multiple wallets to cover their tracks. AML tools analyze blockchain activity, flag unusual wallet behavior, and screen wallets against sanctions lists to stop fraud in its tracks.

Brokerages

Brokerages face risks from money laundering schemes disguised as securities trading or market manipulation. Criminals can layer funds across accounts, trade illiquid assets, or inflate stock prices. AML systems catch unusual trading behaviors and block illicit activities before they escalate.

Insurance providers

Insurance policies are an unexpected yet effective laundering tool for criminals. Overfunded policies, early surrenders for clean payouts, and fraudulent claims are common tactics. AML tools detect irregular premium payments, early cancellations, and claims tied to suspicious entities or individuals.

Legal firms

Legal firms aren’t immune — escrow services and client privileges can be misused to hide illicit funds. AML systems identify unusually high escrow deposits, track frequent ownership changes in deals, and help law firms stay compliant without compromising client trust.

Key targets of AML transaction monitoring

Money laundering

Terrorist financing

Fraud

Drug trafficking

Human trafficking

Identity theft

Bribery & corruption

Sanctions evasion

Tax evasion

Who needs AML transaction monitoring?

Banks

Money transfer services

Wealth and investment management firms

Lending companies

Currency exchanges

Cryptocurrency platforms

Brokerages

Insurance providers

Legal firms

AML transaction monitoring: what’s next

To deal with money laundering effectively, AML can’t just play catch-up — it needs to get ahead of the game. The future of AML transaction monitoring will be defined by proactive, integrated approaches designed to tackle the challenges of increasingly sophisticated financial crime.

Intelligence-led risk management

AML monitoring will adopt a smarter, proactive approach, dynamically adjusting controls to target high-priority risks while minimizing effort on lower-risk areas through a risk-based approach.

Proactive and collaborative FIU

Financial Intelligence Units will focus on disrupting serious financial crime, identifying emerging threats, and collaborating with public and private entities for stronger, faster impact.

Convergence of monitoring capabilities

AML, fraud detection, cybersecurity approaches, and sanctions monitoring will converge into integrated systems, providing a holistic view of risk and enabling focused investigations on high-priority cases.

Integrated data and technology infrastructure

A unified, cloud-based infrastructure will enable seamless data sharing, while AI/ML will identify complex criminal patterns, driving both accuracy and efficiency in detecting financial crime.

Dynamic customer lifecycle management

Continuous customer due diligence (CDD) will use AI and ML to monitor clients throughout their lifecycle, responding to risk triggers and significant changes with precision and speed.

Integrated AML operations

Dynamic and interconnected operations will unify insights from AML, transaction monitoring, fraud detection, and sanctions screening to enable a smarter, more efficient response to evolving financial crime threats.

Future-ready AML transaction monitoring

Intelligence-led risk management

Dynamic customer lifecycle management

Convergence of monitoring capabilities

Integrated data & tech infrastructure

Proactive and collaborative FIU

Integrated AML operations

Closing thoughts

Fighting financial crime is a never-ending battle. While we’ve learned a lot and built solid AML transaction monitoring solutions, staying ahead means being flexible, proactive, and taking a comprehensive approach. It’s the only way to keep your business safe, your transactions secure, and your customers protected.

Payment screening is a one-time pre-transaction process that checks payments against historical risk databases. In contrast, transaction monitoring is an ongoing process that analyzes post-transaction activities as well to detect broader suspicious behaviors.

KYC is key to spotting high-risk customers, like those tied to sanctions, politically exposed persons (PEPs), or shady industries. It also prevents identity theft and synthetic fraud by stopping criminals from using stolen or fake identities to exploit financial systems.

Each country has its own regulatory frameworks for AML, like the BSA and USA PATRIOT Act in the US or 5AMLD and 6AMLD in the EU. However, the main requirements remain consistent: risk-based monitoring, customer due diligence, and reporting suspicious activities to the relevant authorities.

AML transaction monitoring systems need regular updates to keep up with evolving financial crime tactics. Best practices recommend reviewing and updating these systems at least annually or whenever significant changes occur, such as new regulations, emerging risks, or shifts in customer behavior.

A deep dive into the frontier deployment engineer role and how FDEs transform experimental AI pilots into secure, measurable, and scalable AI production systems.