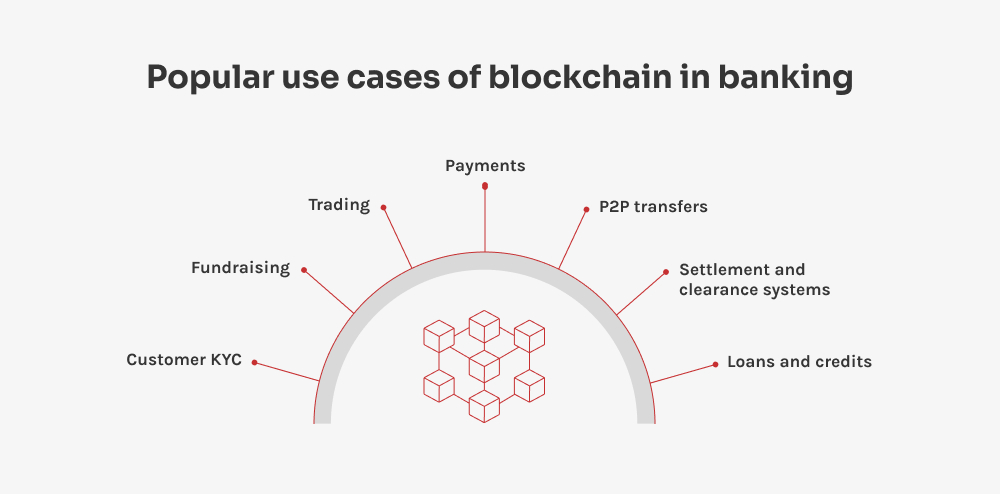

The versatility of this tech means there are a huge number of different blockchain applications in banking – each addressing a specific pain point. Let’s explore some of the most impactful ones.

Payments

One major opportunity for blockchain to shine is in international financial transactions, especially for cross-border payments. Traditionally, these payments involve multiple intermediaries like correspondent banks, as well as lengthy processing times and potential losses due to foreign currency exchange risks. Currently, billions of dollars are wasted due to extra fees and slow payment processes. For instance, sending money from New York to Tokyo can involve both the sending and receiving banks charging around $25 each as a flat fee.

These unnecessary charges can be eliminated with blockchain-based banking payments using cryptocurrencies like Ripple. Crypto payments are quick and straightforward — with no surprise transaction fees. If that wasn’t enough, blockchain decentralization means there’s no need for third-party verification, speeding up and reducing the cost of transfers.

P2P transfers

Similarly, P2P payments have changed the way individuals transfer money — making it easy for users to send funds in just a few taps. All that’s needed is the recipient’s email address or phone number — meaning splitting bills with friends and family has never been simpler. Say you go out for dinner; you can pay your friend right back by selecting their name in your app, entering the amount, and hitting send.

Once your friend receives the money, they can either keep it in their P2P account or transfer it to their bank. With blockchain, this process is even better: it cuts out the middleman — bypassing traditional banking networks, cutting down on unwanted fees, and increasing security. This keeps hackers at bay and ensures that P2P payments are carried out fast and at minimal cost.

Settlement and clearance systems

Moving on to something a bit more complicated: how blockchain is set to improve settlement and clearance processes, traditionally riddled with inefficiencies. Right now, banks are stuck with a messy web of intermediaries and manual processes, leading to delays and errors. The SWIFT network processes millions of requests a day, but many still need some level of manual intervention. Blockchain offers a solution by making direct settlements possible — all while providing transparent, real-time views of transactions. This not only accelerates the process but also reduces costs and minimizes errors.

Loans and credits

Another area where blockchain really shines is loans and credits. In the old-school lending world, banks tend to assess risk using centralized credit reporting systems, looking at factors like credit scores and debt-to-income ratios. The process may be inefficient and opaque, which may adversely affect the consumer. Blockchain in banking brings a decentralized approach to the table — creating a transparent and unchangeable record of your financial history. This means banks can make quicker, better-informed lending decisions — plus this tech streamlines loan processing by automating credit assessments and reducing reliance on outdated data from credit agencies.

SoulBound tokens make a big difference here. Imagine these tokens as a digital way to carry your credit history securely with you, wherever you go. They’re not something you can just trade or give away, as they’re tied to your identity. If you switch banks, your new bank can simply check your SoulBound token and get a sense of your creditworthiness right away. This makes everything much more straightforward — not just for you but for the banks too. By leveraging blockchain, banks speed up the approval process and also democratize access to financial services — helping more people get the loans they need.

KYC

Speaking of efficiency, the know your customer (KYC) protocol is another crucial use case in the financial sector. It’s especially beneficial for banks and FinTech companies onboarding new customers. This process typically involves collecting sensitive data such as names, addresses, and government IDs to comply with regulatory standards and screen against sanctions lists. The banking industry spends millions annually on these efforts —which, unsurprisingly, can be pretty slow and clunky — particularly when it comes to manual document reviews.

Blockchain technology offers a solution that securely stores customer data on a decentralized network — slashing the time and resources needed to monitor and speed up access to data. Blockchain technology in banking is shaking up the sector by creating customer profiles that can’t be changed once set and can only be accessed by people who have the right permissions – helping banks stay on top of regulations without breaking a sweat.

SoulBound tokens also play a crucial role in the KYC process and make things smoother. These tokens act like a secure, non-transferable digital ID that stores your verification details — meaning banks and FinTech companies can confirm who you are quickly without having to ask for your details over and over. This streamlines the whole process — saving time while keeping your information safe and while ticking those important security and legal boxes.

Fundraising

Blockchain tech is shaking up the existing fundraising landscape — especially for startups, charities, political campaigns, government groups, and crowdfunding platforms. By using blockchain, these entities can utilize a decentralized platform that not only gathers but also converts various fiat currencies into one consolidated crypto fund for disbursement. This method enhances transparency and security, ensuring that all transactions are traceable and immutable.

The use of blockchain in fundraising reduces the overhead costs associated with managing funds and minimizes the potential for fraud — making it an attractive option for both organizers and contributors. Additionally, blockchain can provide faster access to funds compared to traditional methods, which is crucial for projects that need quick funding to get started or continue their operations.

Trading

Last but not least, blockchain simplifies the trading of assets through decentralized ledgers — cutting out the need for traditional intermediaries like brokers or clearinghouses. Fewer middlemen mean lower transaction fees and faster trade execution — plus everyone can see the transaction history, which builds trust and keeps things reliable. Furthermore, the immutable nature of blockchain records means that once a trade is made, it cannot be altered, which reduces the risk of fraud. As blockchain continues to be integrated into trading platforms, it enables more fluid and straightforward transactions, fostering a more dynamic and accessible market environment.

Imagine almost all banking operations — from managing accounts to processing payments — being replaced by smart contracts, especially in areas like interbank settlements. Smart contracts are great at managing a high volume of small transactions really efficiently — automating routine tasks and beefing up security, drastically cutting down on manual labor and reducing the margin for error in the meantime.